Nearly 20% of 401(k) participants have an outstanding plan loan, according to the Employee Benefits Research Institute, despite the widespread advice to leave these funds untouched until retirement. While it’s certainly ideal to keep your nest egg vested until retirement, retirement plan loans aren’t necessarily a bad idea for those who require easy access to short-term liquidity—especially when there is a bear market. Let’s take a look at whether you can borrow from your retirement plan, various pros and cons, and alternatives to consider.

Retirement Plan Loan Regulations

The IRS permits most employer-sponsored retirement plans to offer loans to participants, but plan sponsors are not required to include loan provisions in their plans. However, Individual Retirement Accounts, or IRAs, such as SEP, SIMPLE IRA and SARSEP plans, cannot offer loans to plan participants under IRS laws. The IRS also doesn’t allow you to take out a loan from a 401(k) that’s still held at a former employer.

The rules surrounding retirement plan loans vary depending on the plan sponsor. For example, some plans only permit loans for what they consider hardship circumstances while others permit loans for any reason without the need to disclose the reason. Some retirement plans also require a participant’s spouse’s written consent if the loan is greater than $5,000.

There are some standard rules that all plan participants must follow:

- Maximum Loan Amount: The maximum amount that a participant may borrow from his or her plan is 50% of his or her vested account balance or $50,000, whichever is less. The only exception is if 50% of the vested account balance is less than $10,000. In that case, the participant may borrow up to $10,000, although plans are not required to include that exception.

- Repayment Requirements: Employees must generally repay a retirement plan loan within five years and must make quarterly (or more frequent) payments. The only exception is if an employee uses the loan to purchase a primary residence.

Retirement plan loans that exceed the maximum amount or violate any rules, such as repayment requirements, will be deemed distributions. You will need to pay taxes on the distribution and could be subject to a 10% early distribution tax if under the age of 59 1/2. These distributions must still be repaid by the employee, and the repaid amounts will be treated as basis and will not be taxable when later distributed by the plan.

When It Makes Sense to Borrow

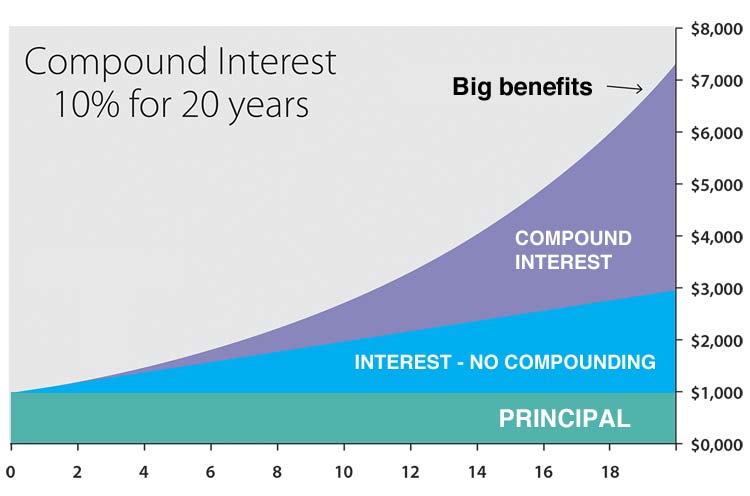

Most people understand the cost of borrowing from a retirement plan. The assets that are removed from your retirement plan account as a loan loss the benefit of tax-deferred earnings growth (e.g. compound interest) until the amount is repaid and the interest on loan repayments are subject to double taxation. Of course, the opportunity cost on the borrowed assets is highest when there’s a bull market.

Download these 7 Tips to Maximize Cash Flow Investing in Your Retirement Portfolio

Chart showing the impact of compound interest over time. Source: Anson Analytics

Despite these downsides, there are some benefits to borrowing from a retirement plan compared to various alternatives. The interest that you repay on a qualified plan loan is repaid to your plan account instead of a financial institution, there’s more flexibility in making repayments and there’s a potential benefit to your retirement savings in a bear market.

You should speak with a financial advisor to consider all of your options before making a decision. For example, serious short-term liquidity needs due to an emergency may necessitate borrowing from your retirement accounts. Keep in mind, all loans must be repaid at the termination of employment in order to avoid taxation and penalty. On the other hand, borrowing from retirement plans to finance the purchase of a new car is usually a bad idea.

Alternatives to Consider

Borrowing from a retirement plan is one way to raise short-term funds, but it’s not the only option available to most people. Depending on your credit rating, home ownership and other factors, you may have access to a wide range of financial products with different pros and cons to consider before making a final decision.

Don’t forget to download 7 Tips to Maximize Cash Flow Investing

The most popular alternatives for short-term loans include:

- Personal Loans: Personal loans are short-term loans from banks, credit unions or private lenders, including online peer-to-peer marketplaces.

- Low-interest Credit Cards: Credit cards can be a valuable source of emergency capital, particularly if they offer low interest rates on unpaid balances.

- Home Equity Line of Credit (HELOC): Homeowners can tap the equity in their home with home equity lines of credit, or HELOCs, that tend to offer low interest rates.

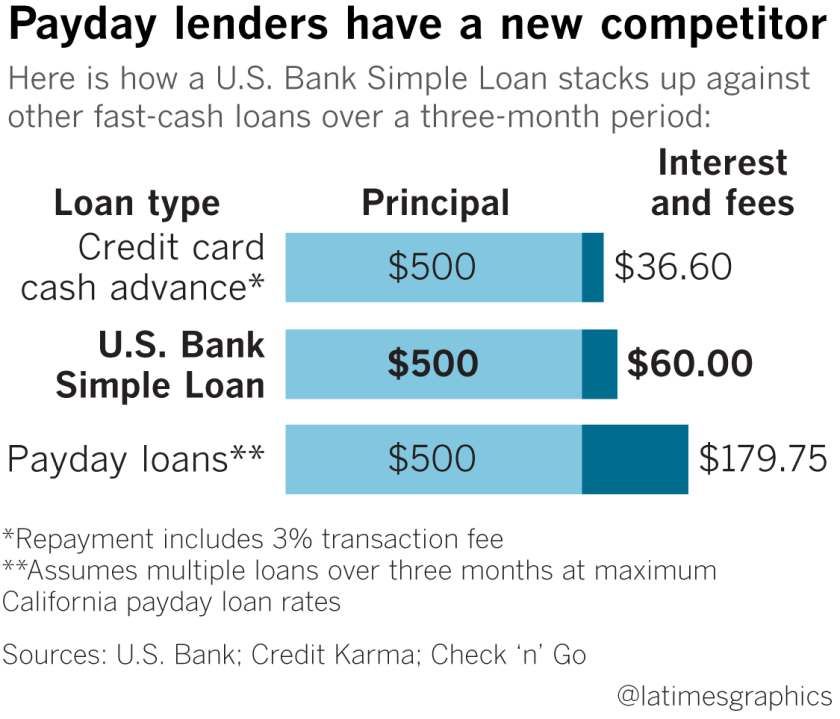

- Payday Loans: Payday loans are extremely short-term loans that are repaid with your next paycheck, although they have extremely high interest rates.

Comparison of interest and fees. Source: LA Times

The 2020 CARES Act also permits qualified individuals to take COVID-19-related distributions of up to $100,000 in distributions from eligible retirement plans (including IRAs) between January 1 and December 30, 2020. Of course, withdrawing retirement savings—even without penalty—could have a significant impact on the growth of your retirement savings. It also allows you to replace the funds over the next three years or spread the taxes over the same time period.

Sign up for a free e-course today or contact us to learn about our asset management options.

The Bottom Line

The best option is to avoid the need to take out short-term emergency loans by maintaining adequate emergency savings before you face an emergency. Most financial advisors recommend saving three to six months’ worth of expenses. While this amount can be daunting to those with little or no emergency savings, you can put away a small amount each week or two to build up to the goal over an extended period of time.

If you don’t have sufficient savings and require a short-term loan, retirement plan loans aren’t a bad option to minimize cost and have greater flexibility with repayments. Keep in mind, most people need loans during economic downturns, potentially the worst time to tap those assets. Selling investments after a steep decline without the ability to participate in a recovery will do permanent damage to a retirement portfolio.