Retirement investors often look for ways to generate income from their existing investments, especially during uncertain economic times. The recent volatility in the stock market spilled over to affect many sectors, especially cryptocurrency.

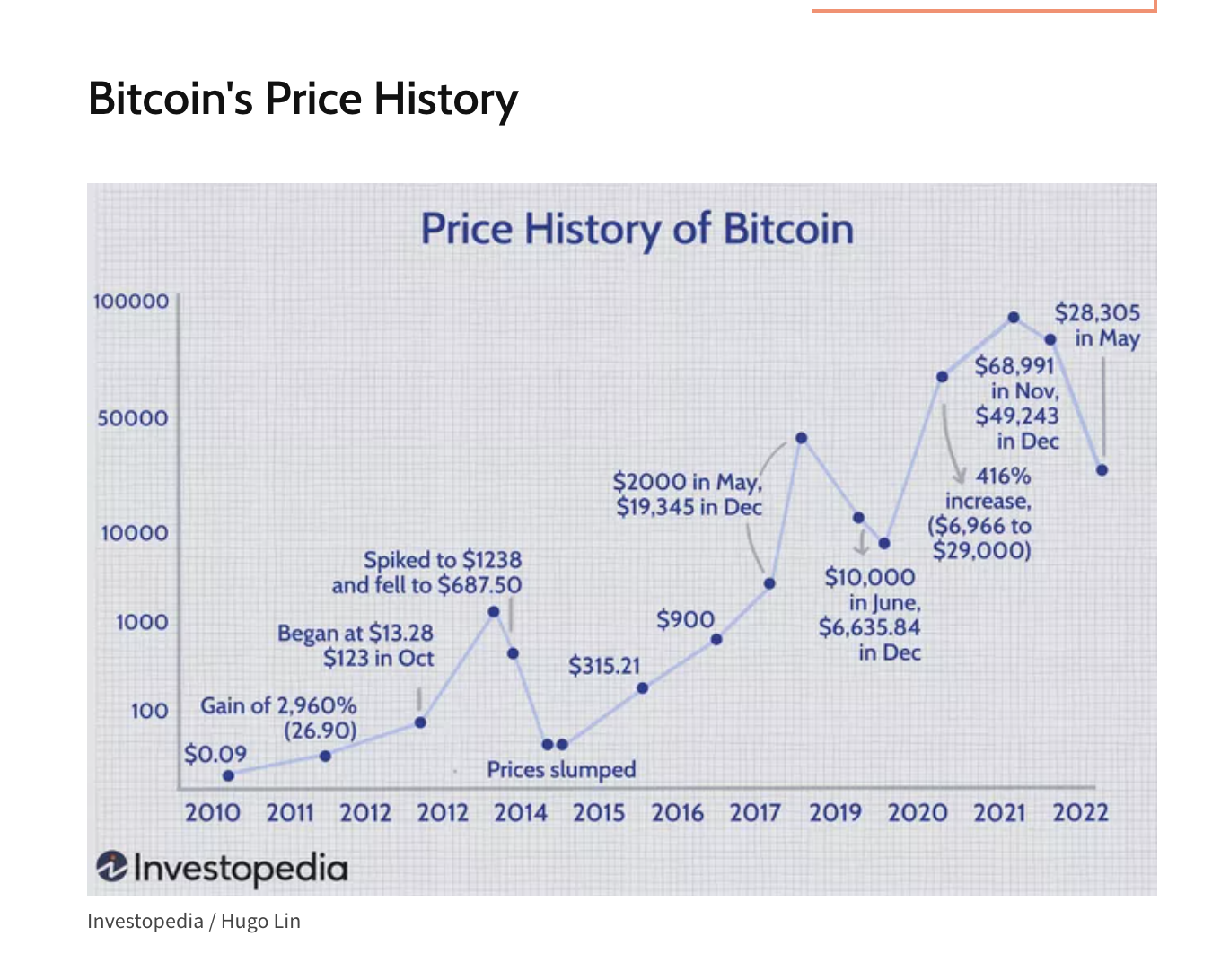

Bitcoin’s inventors launched cryptocurrency as a concept in 2009 as a possible alternative to prevent another 2008 financial meltdown. Bitcoin and other digital coins didn’t start gaining much momentum as an asset class until about 2011. The value of bitcoin has risen over time, but it has not been smooth sailing. The cryptocurrency space has seen some pretty spectacular ups and downs.

(source)

While this post will look at the pros and cons of cryptocurrency as part of a retirement plan, the bottom line is that with any unregulated investment, you should never invest more than you can afford to lose

Cryptocurrency as an Asset Class

Mainstream interest in cryptocurrency reached new levels in 2021. A survey by TurboTax reports that 51% of Americans who own cryptocurrency bought it in 2021. Much of this was due to the rising popularity of Ethereum, the second-largest cryptocurrency by market capitalization.

Bitcoin’s price over the last few years reflects its volatile evolution, from an all-time high of $67,566.83 on Nov. 8, 2021, before it dropped with a thud in 2022 and is now hovering well below $25,000 consistently.

But what exactly is cryptocurrency? Cryptocurrency is a digital or virtual currency that uses cryptography for security. Cryptocurrencies are decentralized, meaning financial institutions do not control transactions and distribution. A distributed network records cryptocurrency transactions on the blockchain, a distributed ledger system that allows for secure, transparent, and tamper-proof transactions.

Investors should note that while Bitcoin’s inventor proposed the blockchain as a ledger for Bitcoin transactions, many industries are developing blockchain use cases that have nothing to do with cryptocurrency.

People may buy and sell cryptocurrency on exchanges. Consumers can also use cryptocurrency to purchase goods and services in some markets. Bitcoin has gained traction in parts of the world where the traditional financial systems don’t work well for lower-income people. In a controversial move, El Salvador’s government adopted Bitcoin as its national currency in 2021.

In other words, cryptocurrency has global traction. However, despite the impressive run-up in 2021, the current dramatic fall from grace proves that cryptocurrencies remain a risky investment.

If you spend time researching cryptocurrency, you will notice that many people have an emotional attachment to certain coins or the ideology of decentralized currency. At Snider Advisors, we encourage investors to leave their emotions at the door when developing investment strategies.

For a more logical view, you can check out the writings of Prof. Steven Schwarcz from Duke University School of Law. He provides a grounded explanation of the relationship between liquidity and volatility in cryptocurrencies.

Apart from the volatility, one of the major cons of investing in cryptocurrency in general, especially for retirement investing, is the speculative nature of the investment. At Snider Advisors, we believe retirees should invest in income producing assets, since income becomes the number one priority when you no longer work. Investors in cryptocurrency seek capital appreciation rather than income. This becomes very harmful to a retiree’s portfolio if they are forced to sell asset for less than what they paid for them in order to meeting living expenses.

Pros and Cons of Cryptocurrency for Retirement

From a traditional retirement investing framework, there aren’t many pros to investing in cryptocurrency or other evolving asset classes for retirement, except perhaps as a small fraction of an overall diversification strategy.

Apart from the volatility risk, the tax reporting requirements for cryptocurrency are also significant. When investing in cryptocurrency, these are some typical tax scenarios:

- Taxable trades and capital gains headaches: Every profitable sale creates a short or long-term capital gain, resulting in taxes owed.

- Taxes on gains result in payments to the IRS: You have less available capital for future investments.

- Devil in the details: Every buy, sell, and swap must be tracked accurately, with cost basis considerations.

Cryptocurrency SDIRAs

For curious investors, a cryptocurrency IRA may be an option. Investing in cryptocurrency through a retirement IRA is one way to solve the dilemma of tax complexity. Consider the difference when you invest in a self-directed cryptocurrency IRA (SDIRA):

- Unlimited trades that do not cause a taxable event.

- Compounding gains rollover within the account year to year.

- No need for complex paperwork tracking because your transactions are not creating a taxable event.

- Tax-free or tax-deferred growth, depending on the type of IRA.

- When you reach the age of 59 ½, you only pay income taxes when you withdraw from a Traditional, SEP, or SIMPLE IRA. You never pay capital gains or income tax on a Roth IRA held for five years or more.

- Investing in cryptocurrency with an IRA means you are not required to report cryptocurrency transactions on your annual taxes. You simply provide contributions made to the account to the IRS. Your IRA custodian helps with other tax reporting. (source)

As you can see, an IRA that invests in cryptocurrency simplifies record keeping and offers tax advantages. However, simplifying tax time still does nothing to minimize the volatility risk and uncertainty in the cryptocurrency market. At this stage of the game, cryptocurrency is more of a gamble than an investment, and we believe no one should gamble with their retirement funds.

Investors should remember that cryptocurrency is still an unregulated asset. Just like the wild west of the past, it attracts many people who take advantage of the ambiguity to create scams and outright fraud.

There are legitimate platforms and most large mainstream investment firms now have a cryptocurrency business unit. Anyone new to space should take their time to get to know the companies and people behind any ventures before forking over their hard-earned fiat.

Other Alternative Asset Classes

For investors looking for alternative ways to generate income from the portfolio with less risk, more established alternative asset classes like hedge funds, private equity, real estate, and commodities.

Hedge funds are pools of capital managed by investment professionals pursuing various investment strategies. Private equity is capital that is invested in privately held companies. Both types of investments usually cater to wealthy accredited investors.

Real estate includes investments in properties or mortgages. Commodities are investments in natural resources such as gold, oil, or agricultural products.

Each of these asset classes has different risk and return characteristics. Investors often allocate a portion of their portfolios to alternative asset classes to diversify their holdings and reduce risk. Investing in various asset classes can mitigate the effects of any one investment performing poorly.

Another investing strategy investors may consider is writing covered call options on stocks in their portfolio to generate premium income. Relative to the ideas above, covered call options require less time and have lower transaction costs and risk, especially compared to cryptocurrency.

The Bottom Line

In the world of unregulated alternative asset classes, cryptocurrency is something of a wild card representing the leading edge of the evolution of finance. There is a lot of uncertainty about how governments will regulate it in the future.

Highly volatile, risky investments generally don’t play a significant role in a sound retirement strategy. Curious investors considering a cryptocurrency investment should remember it is unwise to invest more than they can afford to lose, even in a cryptocurrency IRA.

Aside from cryptocurrency, investors can take advantage of many options to create a custom approach to earning retirement income in 2023, including generating income from an existing long stock portfolio using covered call options.

If you are new to options, the Snider Investment Method provides a time-tested way to find and execute these trades.