The COVID-19 pandemic caused severe disruptions to the global economy, but the economic consequences of the pandemic could last far more than a year or two. With massive job losses in major economies worldwide, many people have been forced to dip into their savings accounts just to survive, which could jeopardize their ability to comfortably retire.

Let’s take a look at a few ways that these dynamics could impact retirement income for years to come and some strategies to help you get back on track.

Record Low Yields

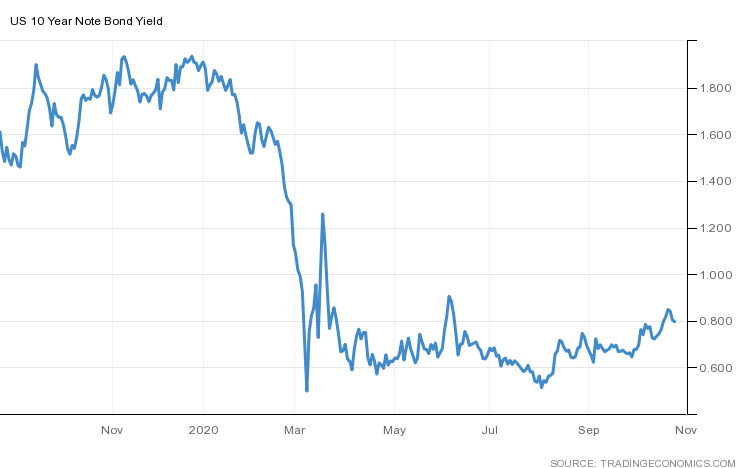

The 10-year Treasury yield—a proxy for market interest rates—fell from a high of 3.25% in July 2018 to a low of 0.53% in July of 2020. In addition to cutting interest rates to 0.25%, the Federal Reserve introduced several bond-buying programs aimed at improving liquidity and keeping bond yields low throughout the COVID-19 pandemic.

10-Year Treasury Bond Yields – Source: TradingEconomics

Unfortunately, many retirees rely on fixed income investments, such as bonds, to generate income during retirement. The significant drop in bond yields means that many of these investors will see a pay cut that forces them to either allocate more capital to bonds or start selling other assets to generate cash flow.

Despite rising fiscal deficits, bond yields are expected to remain low for at least the next several years due to the lack of underlying economic growth. Central banks don’t want to raise rates because lower interest rates incentivize spending while weak demand could create more of a risk for deflation or disinflation than inflation over the intermediate term.

Forced Early Retirement

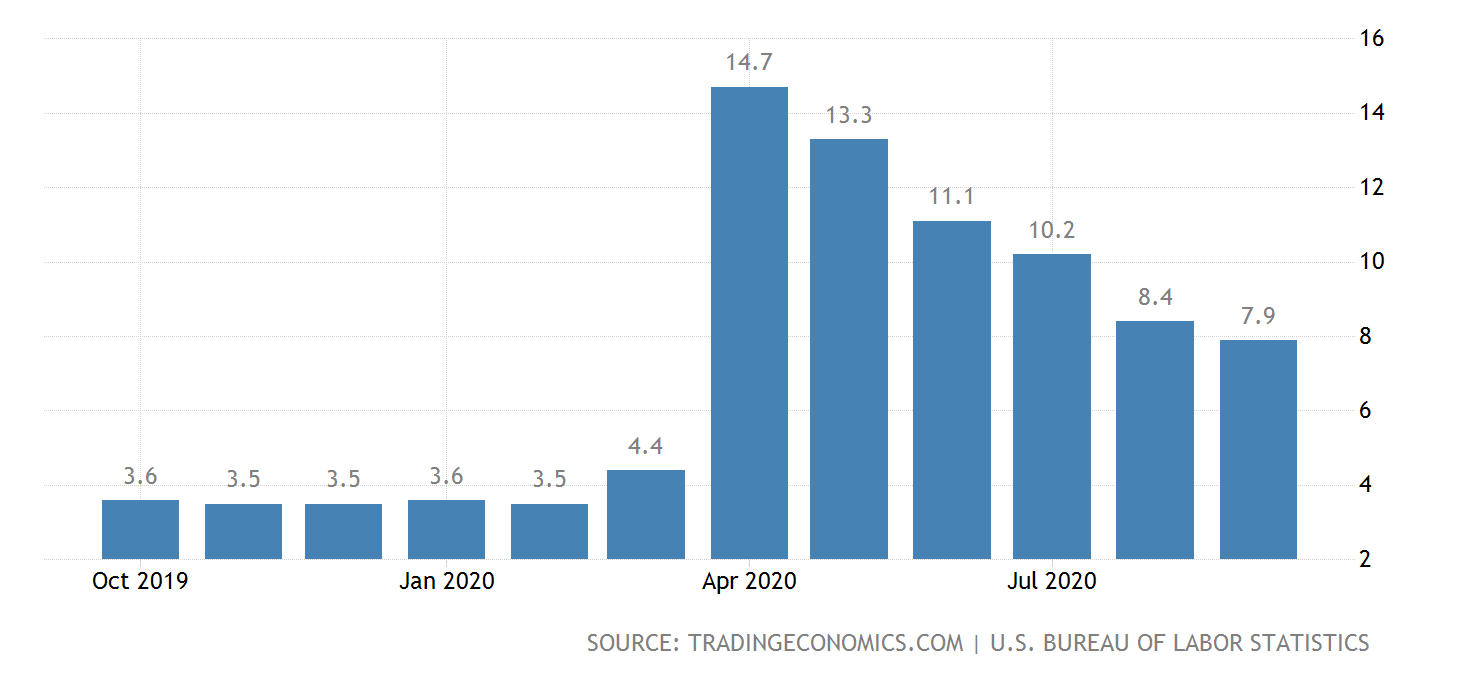

The U.S. lost more than 20 million jobs between March and May with unemployment levels surpassing 14%—their highest since the Great Depression in the 1930s. While most of these jobs are expected to return when the pandemic recedes, some jobs may never return and many workers near retirement age have opted to take early retirement.

U.S. Unemployment Rate – Source: TradingEconomics

Many people forced into early retirement are taking Social Security benefits earlier than they normally would, which permanently decreases their lifetime income from the program. For instance, taking Social Security at 62 years old reduces your benefit by up to 30% while delaying Social Security until 70 years old results in an additional 24% in benefits.

In addition to early Social Security, leaving the workforce before reaching full retirement age can put a strain on your lifetime retirement income. Many people generate retirement income through a combination of portfolio income and capital gains from sales. Of course, these sales deplete a portfolio over time and extending the time in retirement puts more strain on your portfolio.

Reduced Retirement Funds

The COVID-19 pandemic has forced many people to dip into their retirement savings, especially as enhanced federal unemployment benefits phase out. Between April and June, ADP found that nearly 20% of all distributions were “coronavirus-related distributions”. Fidelity also found that 3% of its plan participants (711,000 people) took an average of $4,800 from their plans.

These distributions are penalty-free after the CARES Act passed in response to the COVID-19 pandemic, but they are subject to income tax over a maximum of three years. In addition to paying these taxes, these individuals may never rebuild their retirement nest egg to its former amount, have less time compounding, and therefore, have less income during retirement.

The impact of these decisions to withdraw retirement funds depends on a person’s age. While younger investors have time to rebuild their nest egg, those that plan on retiring in the near-term will likely face a permanent decrease in their retirement income that will be difficult to recoup without taking on an extra job or other measures.

How to Boost Retirement Income

There are many different ways to generate income from a portfolio, from low-risk Treasury bonds to higher risk option strategies. Of course, each strategy involves its own pros, cons and risk-adjusted returns. Investors must consider how each fits within a larger portfolio.

The most popular bond alternatives include:

- Dividend Stocks: Many stocks pay dividends to investors, particularly utilities and defensive stocks. These stocks enable investors to generate income while maintaining a long stock position, although the stock can decline in value over time. TrackYourDividends is a great tool to monitor dividend portfolios.

- Energy MLPs: Pipeline operators are typically structured as Master Limited Partnerships, or MLPs, that charge energy companies a fee for distribution and distribute almost all of those gains to shareholders.

- High Yield Bonds: High yield bonds provide greater yield than conventional government or AAA-rated bonds, but they typically have a higher risk of default. Investors must carefully assess these risks before investing in these riskier bonds.

- Real Estate: Real estate investments generate income in the form of rental income. While it’s possible to invest in real estate independently, many investors prefer to invest in REITs or eREITs to offload the management responsibilities.

- Stock Options: Stock options enable investors to generate income in the form of option premiums. Depending on the strategy, options can be a relatively safe strategy or an extremely high-risk strategy, so it’s important to understand what’s happening.

The Snider Investment Method generates income from an existing long stock portfolio using covered call options. By selling the right to purchase stock that you own at a higher price, the strategy generates income from option premiums that may be greater than the yields offered by many fixed income alternatives, particularly when factoring in the risk.

The Bottom Line

The COVID-19 pandemic could permanently decrease retirement income due to lower yields, early retirement or depleted retirement nest eggs. Fortunately, there are a few ways that those affected by the pandemic can cope with these challenges and boost their income prospects during retirement to come out the other side without a problem.

Sign up for our free e-course to learn more about covered calls and how they can help you generate more income during retirement.