As you may have heard, the Federal Reserve plans to raise interest rates over the next two years. While the central bank hiked rates to 2.25% to 2.5% in July, the futures market predicts these rates will be even higher a year from now. Aside from a brief period in 2019, rates haven’t been that high since before the 2008 financial crisis.

Let’s look at what factors influence interest rates and how various investments perform when rates rise.

Why Interest Rates Rise

Suppose that a friend wants to borrow $10,000 to start a business. The amount of interest you charge them would depend on several factors, such as how much you have in the bank, what other opportunities you have to invest in, or even what inflation might look like next year. As you can see, there are a lot of factors that affect interest rates.

The three main factors influencing national interest rates include:

- Supply and Demand – Lenders increase interest rates when there’s a higher demand for credit to maximize their return on capital. E.g., If ten friends want to borrow money from you, you can increase your interest rate to earn the most from the demand.

- Federal Funds Rate – The Federal Reserve sets the interest rate that institutions charge for ultra-short loans. They can also buy and sell government securities, influencing the amount of capital in the economy that’s available to lend out.

- Rate of Inflation – Lenders repaid over long periods increase interest rates when inflation rises to offset the reduction in purchasing power. If a dollar is only worth 90 cents in a year, they want to ensure they make up the difference.

After the COVID-19 pandemic began, federal stimulus and spending flooded the economy with credit. Meanwhile, supply chain disruptions have pushed up consumer product prices, and Russia’s invasion of Ukraine pushed oil prices past $100 per barrel for the first time in years. These factors have culminated in soaring short-term inflation.

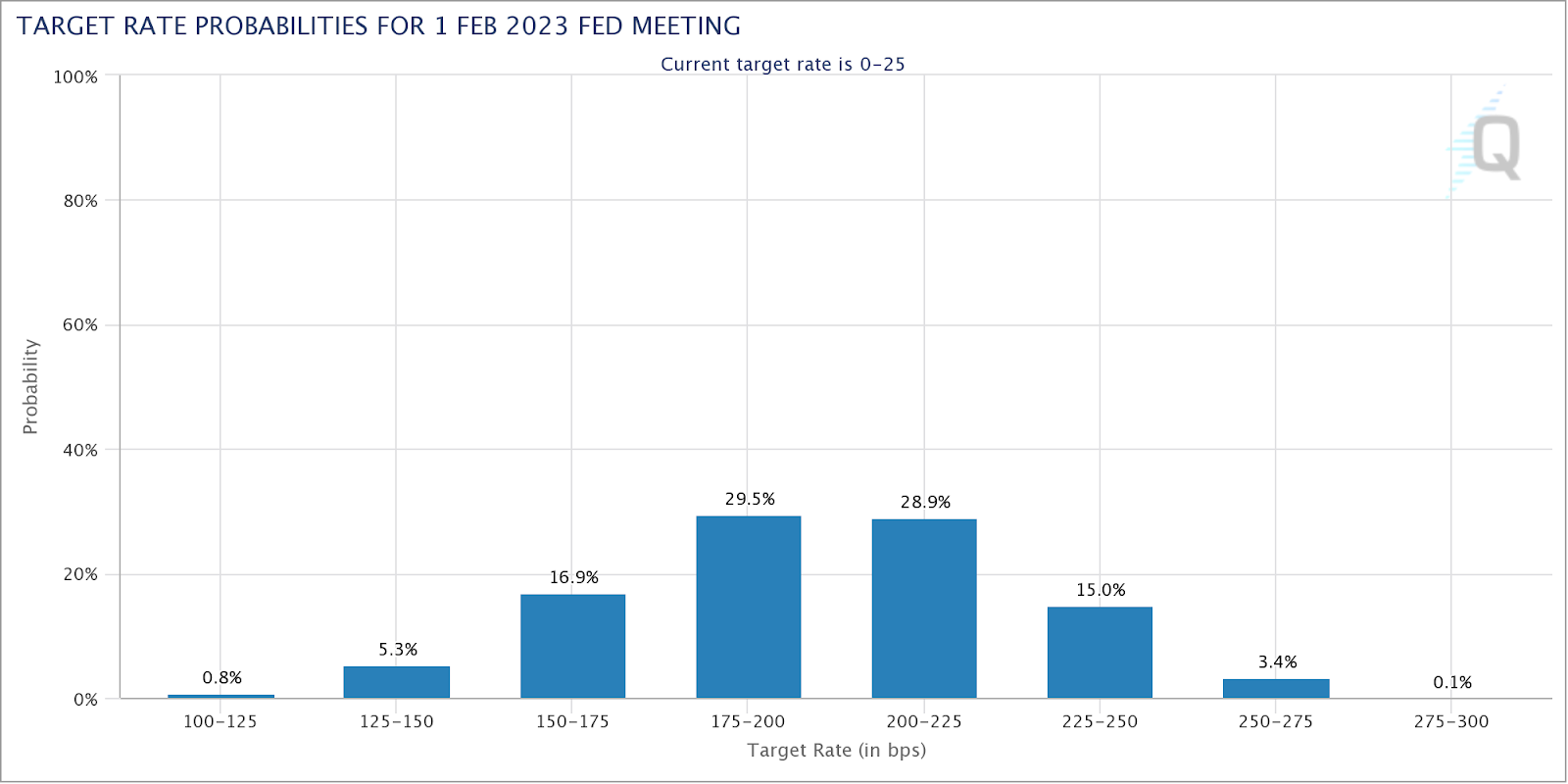

The CME’s FedWatch Tool shows where the futures market expects the Fed Funds Rate to land at each meeting. Source: CME Group

The Federal Reserve announced plans to raise interest rates to tame inflation while lenders are raising interest rates because they expect less purchasing power in the future due to inflation. As a result, the futures market predicts that interest rates will rise in the intermediate-term but remain at around 2.25% to 2.75% through the middle of 2023.

Finally, it’s important to keep in mind that inflation and interest rates aren’t the same. In fact, higher interest rates are designed to reduce inflation by reducing borrowing and, therefore, spending. That said, rising inflation usually leads to higher interest rates as the central bank attempts to address the problem.

Investing with Rising Rates

Rising interest rates tend to be bearish for stocks and bonds. While they’re usually a sign of a strong economy, they have a cooling effect on economic growth and adversely impact fixed-income investments.

Higher interest rates result in lower bond prices because investors sell bonds locked into lower rates to invest in new bonds at higher rates—and that selling pressure sends prices lower. Meanwhile, higher interest rates reduce borrowing and slow down the economy, resulting in fewer earnings and lower multiples for stocks—resulting in lower prices.

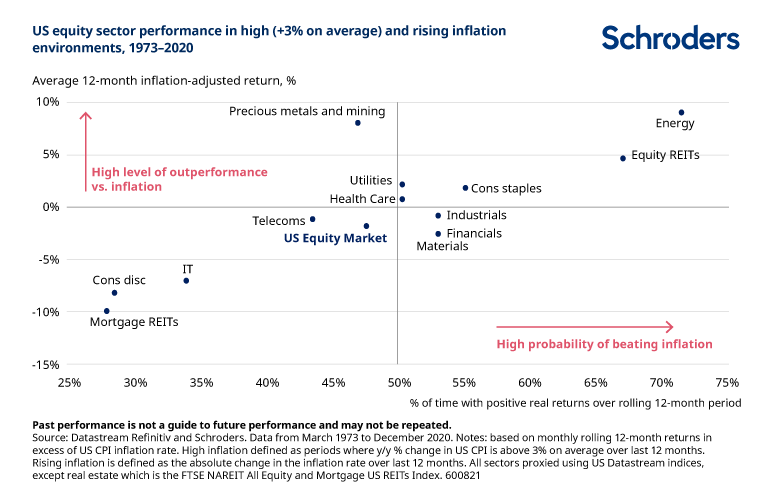

Schroders looks at the sectors best and worst positioned to beat inflation. Source: Schroders

The financial sector is usually a significant beneficiary of rising interest rates. Banks profit from the difference between what they pay depositors and charge borrowers—or the net interest margin. When interest rates rise, they can charge borrowers more without necessarily increasing depositor interest rates in the short term.

Real estate investments also tend to perform well when interest rates rise. With long-term mortgages in place, they have a steady monthly interest payment. However, they can raise rental rates to adjust for increasing inflation, generating a higher return on assets for owners. That said, mortgage rates tend to suffer the most from rising rates.

On the other hand, information technology and consumer discretionary stocks suffer the most. That’s because growth stocks are valued based on their future cash flows. If that future money is worth less due to inflation or opportunity cost, investors aren’t willing to pay as much for them, reducing their earnings multiples and prices.

Hedging Your Portfolio

Most investors have target asset allocations reflecting their long-term goals. For instance, investors in retirement might have 80% of their capital in bonds and 20% in stocks. Their goal might be to maximize income from bond payments while minimizing volatility from equities. But, of course, higher interest rates could throw a wrench into these plans.

A common solution is hedging the portfolio against rising interest rates. Rather than selling bonds, the investor could preferentially hold bonds with shorter durations that react less to changes in interest rates. At the same time, they might shift their equity portfolio into financials, real estate, or other inflation-protected industries.

Others may consider alternative strategies to generate income without the risk of holding bonds. For instance, covered calls enable investors to generate income from blue-chip equities above and beyond dividends. The Snider Investment Method provides an easy-to-use system for managing these trades to maximize income and minimize risk.

Take our free e-course or inquire about our asset management services.

The Bottom Line

Interest rates are likely to rise over the coming year as the Federal Reserve moves to combat rising inflation. As a result, investors may want to start thinking of ways to hedge their portfolios against losses by moving into inflation-resistant securities.

To learn more about covered calls, take our free e-course that discusses how covered calls work and tips for using them. You can also use our free covered call screener to find opportunities for your portfolio.