The Consumer Price Index rose 7% in 2021 and came in at 8.5% over the last 12 months in March, marking it the fastest pace since 1982, according to the Labor Department. While consumers are already feeling the effects of inflation, financial assets are only beginning to react following the Federal Reserve’s move to raise interest rates—and these movements are starting to worry investors.

Let’s look at how to think about inflation, its effect on different assets, and how investors can hedge against losses.

What is Inflation?

Most people understand that inflation results in higher prices, but fewer know how inflation works under the hood. By understanding the root cause of inflation, you can better assess its long-term impact and maximize the effectiveness of inflation hedges. In particular, you can better predict if it’s a temporary or long-term problem.

There are two types of inflation:

- Demand-pull inflation occurs when aggregate demand increases faster than aggregate supply. Since market equilibrium determines the market price, higher demand translates to higher prices.

- Cost-plus inflation occurs when the cost of raw material, labor, and other inputs rises. If producers want to maintain profit margins, they must pass on these costs to customers via higher prices.

Most long-term inflation comes from lax monetary policy that increases the money supply relative to the size of the economy. However, short-term inflation might come from supply shocks that disrupt production, demand shocks that provide consumers with a windfall, or expansionary economic policies, such as lowering interest rates.

Expectations also play an essential role in determining how inflation plays out. For example, if people expect prices to rise, they tend to negotiate higher wages or build price increases into contracts, like rental agreements. The result is higher payroll costs for businesses or housing costs for renters, making inflation self-fulfilling to some extent.

Finally, it’s crucial to realize that inflation isn’t inherently negative. After all, persistent deflation leads customers to put off purchasing decisions in anticipation of lower prices in the future, leading to less economic activity. As a result, most economists agree that a 2% annual inflation rate is ideal for preserving wealth and maximizing economic growth.

Measurement & Response

Inflation is a challenge to measure because people purchase various goods and services. For example, a sharp increase in gas prices translates to a lot more inflation for someone who commutes an hour each way to work than it does for someone taking public transit. Actual inflation varies per individual or business.

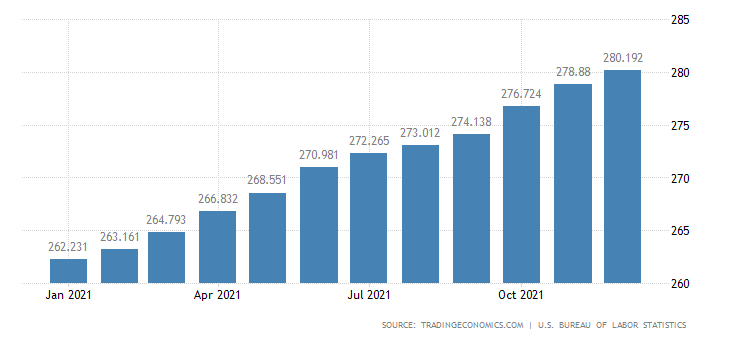

The U.S. government measures inflation using the Consumer Price Index, or CPI. With data from household surveys, the government identifies a basket of commonly purchased items and tracks the cost of purchasing them over time. Starting from a base year, the CPI is adjusted higher or lower depending on these changes in prices.

U.S. Consumer Price Index – Source: Trading Economics

The government also tracks Core Consumer Inflation by removing certain volatile products like food and energy from the CPI. That’s because these products are subject to seasonal factors and temporary supply conditions that may yield misleading CPI data. The result is a steadier look at long-term inflation without potentially-misleading volatility.

Governments fight inflation with various deflationary policies, depending on the underlying cause of the inflation. The most common policy response is higher interest rates, reducing credit supply to the economy. In addition, many central banks try to influence inflation expectations by announcing interest rate targets or previewing future actions.

Impact on Investments

Inflation has the most significant impact on assets that provide fixed, long-term cash flow. When there’s inflation, the purchasing power of those cash flows declines over time, and the net present value falls. On the other hand, commodities and assets with adjustable cash flows tend to perform better during inflationary periods.

Here’s how some of the most popular assets perform:

- Bonds and other fixed-income investments usually suffer when inflation is on the rise. After all, rising inflation erodes the purchasing power of bonds’ fixed coupon payments. Shorter-term and higher-yielding bonds don’t suffer as much because the term is much less and there’s a larger buffer.

- Equities tend to hold up well against inflation over the long term. Larger companies usually perform better because they can easily pass on price increases, whereas foreign stocks perform worse because of currency conversions. That said, stocks aren’t the most effective inflation hedge.

- Commodities typically perform well during inflationary periods because their dollar value increases as their absolute value holds steady. However, commodities are usually more volatile than other asset classes, and they don’t generate any income, which could be problematic for retirees that require cash flow.

- Real estate is another top-performing asset during inflationary times since it’s easier to raise rental rates than the price of consumer discretionary goods. And unlike commodities, real estate generates a monthly income through rents, making it a good alternative for retirees that need income.

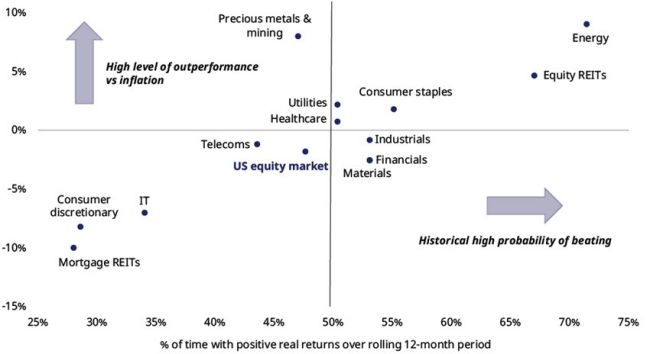

U.S. Equity Performance During High or Rising Inflation – Source: Hartford Funds

Fortunately, there are several ways to hedge against inflation or offset any decrease in real income.

Some of the most popular strategies include:

- Covered calls provide investors with extra income from their equity portfolios, offsetting a decrease in real income (e.g., inflation-adjusted income) from fixed-income.

- Lowering duration can help protect fixed-income portfolios from inflation by reducing exposure. But, of course, the trade-off is investing in higher-risk bonds or accepting lower interest rates due to the shorter term.

- Inflation-protected securities, such as TIPS or Series I Bonds, automatically adjust interest rates to account for changes in inflation, preserving real income levels.

- Dividends are the most common way to generate income from an equity portfolio. Historically, dividend growth has exceeded the long-term inflation rate. This means that dividend-focused portfolios can provide an income that keeps pace or exceeds the inflation rate.

The Bottom Line

Inflation has been on the rise in the U.S. over the past year, but investors are just starting to feel the impact. By understanding the root causes of inflation, it’s easier to identify an appropriate hedge and protect your portfolio from erosion. In most cases, the best response is shifting asset allocations and boosting income through things like real estate exposure or covered calls.

If you’re interested in using covered calls to hedge against inflation, Snider Advisors provides free e-courses and asset management services.