Many retirement-aged investors rely on dividend income to supplement their Social Security, pensions, and other income. In 1978, two-thirds of companies on the NYSE, NASDAQ, and AMEX paid dividends, but those figures fell to just one-in-five companies by 1998 as investors sought out less profitable companies focused on growth.

George W. Bush introduced the 2003 Dividend Tax Cut to encourage more companies to pay dividends. If investors met specific criteria, they would owe no more than 20% tax on the income instead of the higher ordinary income tax rate. Investors should understand these differences to ensure they’re minimizing their tax burden.

Let’s look at qualified dividends, ordinary dividends, and other types of dividends and how they’re taxed.

What Are Qualified Dividends?

Most domestic companies offer qualified dividends to investors that hold their shares for more than 60 days during the 121-day period that begins 60 days before the ex-dividend date—or the cut-off point to receive a dividend payment. In other words, long-term investors that aren’t just trying to capture dividends can pay lower tax rates.

Let’s take a look at a quick example. Imagine a company you’d like to own declares its first dividend. You decided to purchase shares before the ex-dividend date to receive the payment. In order to trigger the lower tax rate on qualified dividends, you must own the shares for at least 60 days. If you sold your shares sooner, the payment would be considered an ordinary dividend with the higher tax rate.

Note: For higher-yielding preferred stock, investors must own the stock for more than 90 days during the 181-day period beginning 90 days before the ex-dividend date.

Qualified dividends have various tax rates:

- High-income earners with a maximum 37% marginal tax rate pay a 20% tax rate on qualified dividends.

- Middle-income earnings with a marginal tax rate of between 15% and 37% pay a 15% tax rate on qualified dividends.

- Low-income earners with a marginal tax rate of less than 15% pay NO tax on qualified dividends.

Qualified dividends are a great way to increase after-tax income for retirement investors. For example, an investor receiving $100,000 per year in ordinary dividends could be paying $17,000 more in taxes each year than they would if they owned qualified dividends. Of course, the benefits are most significant for high-income earners with higher tax brackets.

What Are Ordinary Dividends?

Ordinary dividends are subject to an investor’s marginal tax rate. For example, an investor with a 37% marginal tax rate will pay a 37% tax on ordinary dividend income. In addition to holding stocks longer, investors may want to avoid certain stocks that automatically trigger ordinary dividends regardless of holding time.

Companies that aren’t eligible for qualified dividends include:

- Money market funds

- Banks, thrifts, and other interest payers

- Real estate investment trusts (REITs)

- Master limited partnerships (MLPs)

- Employee stock ownership plans

- Foreign corporations

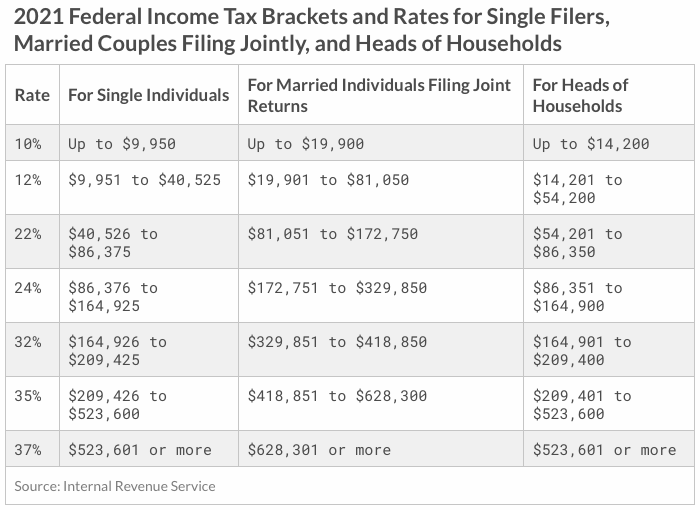

2021 Tax Brackets – Source: Tax Foundation

Of course, there are some instances where investors may find it worth it to pay ordinary dividend tax rates. For example, REITs and MLPs may offer higher dividend yields than comparable dividend stocks while providing valuable diversification to a portfolio. These benefits may outweigh the added tax obligations.

Paying Taxes on Dividends

Most dividend-paying companies issue you a Form 1099-DIV at the end of each year, which specifies whether the dividends were qualified or ordinary. While the determination is automatic, it’s a good idea to understand your dividend tax rates to help with tax planning since dividend taxes are usually year-end cash expenses.

Tax-advantaged accounts enable you to avoid paying taxes on dividends until retirement. For example, if you hold dividend stocks in a Roth IRA, you don’t owe any tax on dividends that you receive and reinvest. Even better, you don’t owe any tax on withdrawals—including dividends—that you take out during your retirement years.

Of course, early withdrawals from tax-advantaged accounts can trigger penalties that create much more significant tax burdens than if you would have stuck to taxable accounts. You also won’t owe any taxes annually on dividends in Traditional IRAs. On these types of accounts, account holders are only taxed on withdrawals.

Investors with a significant amount of dividend income can also reduce their tax burden using tax-loss harvesting. You can offset capital gains or up to $3,000 in ordinary income by realizing losses in losing positions. The catch is that you cannot reinvest in the same or similar securities right away, complicating diversification and asset allocations.

Other Types of “Dividends”

Ordinary and qualified dividends aren’t the only types of cash distributions made to shareholders. As mentioned earlier, some companies pay out royalty income, rental income, interest payments, or make other types of payments to their shareholders. Each of these payments is subject to its own tax rates depending on various factors.

- Return of Capital: Distributions that qualify as a return of capital aren’t dividends. Instead, it reduces the adjusted cost basis of your stock, thereby increasing future capital gains potential.

- Capital Gains Distributions: Short-term and long-term capital gains distributions typically occur in mutual funds. These distributions are subject to the same tax rates as conventional capital gains.

- Interest Payments: Many bonds and other securities make interest payments, typically subject to ordinary income tax, such as a Certificate of Deposit or a corporate bond.

A popular way to generate tax-free cash distributions is through the use of municipal bonds. Many muni bonds are exempt from federal income tax, and bonds in your home state may also be exempt from state tax. While most general obligation bonds have relatively low yields, revenue bonds are riskier and offer higher yields (and potential income). In many cases, the tax advantages of municipal bonds are only useful for the highest tax brackets.

Investors looking for an income boost in addition to dividends in retirement may want to consider covered calls and cash secured puts. For example, the Snider Investment Method uses covered call options to generate a yield on a portfolio of stocks that goes above and beyond dividends. Sign up for our free e-course to learn more or inquire about our asset management services.

The Bottom Line

There are many different ways that companies distribute capital to their shareholders. Understanding the differences between these strategies is essential to minimize your tax burden and maximize your retirement income. Taxes are an important consideration in your investment strategy, but they should be a secondary factor when deciding to buy or sell a security. If you need help minimizing taxes, it helps to engage a financial advisor that’s familiar with your unique situation.

If you are a dividend investor looking for a tool to follow the performance, payments, and diversification of your dividend portfolio, please check out TrackYourDivdends. This is a great tool for dividend investors.