It’s easy to see that many financial assets are highly correlated — especially large assets. If there is a new sign of an economic slowdown, investors expect the entire S&P 500 index to move lower in response. Similarly, if interest rates rise, investors expected all fixed income investments to fall. The individual stock or bond doesn’t really matter, but asset allocation can be beneficial.

Researchers have found that asset allocation accounts for about 88% of volatility and returns. If your portfolio consists of 90% large-cap U.S. stocks and 10% high-yield corporate bonds, your experience in the market will be very consistent with investors holding the same allocation — even if the specific stocks and bonds held in each portfolio are different.

Let’s take a look at asset allocation, different asset classes and what it means for your portfolio.

What Is Asset Allocation?

Asset allocation is the distribution of asset classes, or groups of financial instruments with similar financial characteristics and market behavior, within a portfolio.

Most volatility and returns can be traced back to asset allocation, which makes it one of the most important considerations when building a portfolio. In fact, most investment and retirement advice is focused on adjusting asset allocation over time, rather than picking specific stocks or bonds, to reduce risk or increase income.

The rising popularity of asset allocation funds is a testament to the importance of asset allocation. Target date retirement funds make it possible for investors to own a single mutual fund that adjusts its asset allocation to minimize risk as retirement approaches, while income funds maintain asset allocations that maximize income.

In addition to deciding on an initial asset allocation, investors must maintain their target asset allocation over time. One asset class could outperform others during any given year, which would increase its portion of the overall portfolio. Investors must rebalance their portfolio to reset to their preferred asset allocation on a regular basis.

Asset Classes & Characteristics

There are many different types of asset classes since there are so many different ways to divide assets. For example, investors can break down assets by their type (e.g. stock versus bond), purpose (e.g. growth versus value), location (e.g. U.S. versus international) or other criteria.

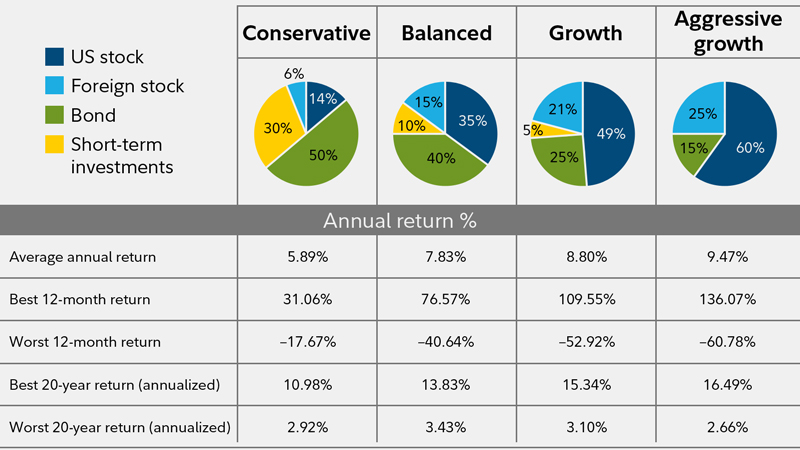

Asset Allocation Examples – Source: Fidelity

Download our Sample Asset Allocation Plans Worksheet for some ideas for structuring your asset allocation.

Stocks/Equities

Stocks, or equities, represent ownership of a publicly held corporation. While they can be volatile short-term investments, they have historically outperformed other investments over the long-term. Most investors hold stocks for long-term capital gains, but many stocks also produce income.

The most significant sub-asset classes of equities include:

- Location – Stocks may be divided into domestic, international, frontier market, emerging market, developed market or other location-based asset classes.

- Size – Stocks may be divided into small-cap, mid-cap, large-cap or other size-based asset classes.

- Strategy – Stocks may be divided into growth, value, income or other strategy-based asset classes depending on the type of corporation and its goals for shareholders.

Fixed Income

Fixed income investments pay a set rate of interest over a given period before returning the investor’s principal. While they are more stable than stocks, they tend to have lower returns than stocks and other riskier asset classes. Most investors use bonds to generate a safe income.

The most significant sub-asset classes of fixed income include:

- Location – Bonds may be divided into domestic, international, or other location-based asset classes, like stocks.

- Issuer – Bonds are often divided into federal, municipal or corporate asset classes based on their issuer.

- Credit Rating – Bonds can be divided into high-grade, mid-grade or junk bond categories based on their credit rating.

Currency

Cash is the most common asset class employed during periods of significant volatility since it’s the least risky asset to own. In addition to cash, investors may use one currency to purchase another currency on the foreign exchange (forex) market to speculate on changes in the relative valuation.

Cryptocurrencies could be another emerging asset class over the coming years, particularly as futures market and exchange-traded funds (ETFs) make them easier to purchase and hold.

Real Estate

Real estate investments consist of a person’s home or investment properties, as well as funds that invest in commercial real estate projects. In addition to the potential for capital gains, real estate investments can produce an income from rents over time.

Commodities

Commodities are physical goods, such as gold, crude oil, wheat or electricity. Many investors build commodities into their portfolios as a hedge against stocks and bonds since they have a relatively low correlation with other assets. However, they are non-income producing by nature.

The most important sub-asset categories of commodities include:

- Precious Metals – Gold, silver, palladium and other precious metals are purchased for investment rather than their commercial use — and they often serve as a safe-haven.

- Energy – Crude oil, natural gas and other energy commodities often experience volatility depending on supply and demand.

How to Decide on an Allocation

Building a portfolio with asset classes may be easier than choosing individual assets, but there are still a lot of different choices to make.

Don’t forget to download our Sample Asset Allocation Plans Worksheet for some ideas for structuring your asset allocation.

There are some general rules that people use to select asset allocations, such as subtracting your age from 110 and putting that percentage into stocks and the rest into bonds. The problem with these generalized approaches is that they fail to take into account an investor’s individual circumstances — such as their individual life expectancies.

The most important thing to remember is to maintain a diversified portfolio with a risk/reward ratio that matches your requirements in retirement and risk tolerance. You shouldn’t take on too much risk that you can’t sleep at night or so little risk that you’ll never have what you need when you retire — it’s a balance.

As your wealth grows, it’s also important to consider non-standard alternatives to see if they’re a better fit than conventional asset classes. For example, income investors may want to consider using covered call options. They can help reduce the risk of the stock portion of your asset allocation. Adding options can also improve the income from equities, reducing your need to rely on fixed income investments to generate an income. The Snider Investment Method provides a streamlined process to generate an options income.

The Bottom Line

Asset allocation is one of the most important decisions that investors must make when building a portfolio. Whether using a financial advisor, target date retirement fund or building your own portfolio to cut out the middle man, the key is building a diversified asset allocation with a risk/reward ratio that matches your requirements and preferences.

A well-constructed portfolio will have at least two asset classes. For most investors, that means stocks and bonds. Until you’ve accumulated significant wealth, there is little need to seek out additional asset classes. It almost never makes sense to bet big on a single asset.

Sign up for our free e-course to learn more about covered call options and how they can help you generate a retirement income without sacrificing the upside potential of stocks.