Retirement is a time for relaxation and enjoying the fruits of your labor, but that doesn’t mean an end to tax and investment planning. In fact, the decisions that you make in retirement can dramatically affect the amount of income that you will receive and how much of a nest egg you have left over to pass on to your heirs.

Let’s take a look at four strategies that you can use to lower your taxes in retirement, as well as some alternatives for generating an income.

#1. Avoid Early Withdrawals

Early withdrawal from an individual retirement account (IRA) prior to age 59½ is subject to being included in gross income plus a 10% additional tax penalty. Plan distributions before age 65 (or the plan’s normal retirement age, if earlier) may result in a similar penalty.

There are some exceptions where you may take distributions without penalty:

- Death or disability

- Qualified higher education expenses

- Qualified first-time home buying expenses

- Certain unreimbursed medical expenses

- Health insurance premiums while unemployed

- Automatic enrollment or equal payments

If you accidentally made an early withdrawal, the IRS penalty abatement program helps first-time offenders reverse certain tax penalties. The only requirements are that you’re current on your taxes and have a clean record over the prior three years.

The best way to avoid early withdrawals is to either defer retirement until age 59½ or take advantage of other sources of income during earlier retirement. For example, you may have taxable accounts or a part-time job until reaching retirement age.

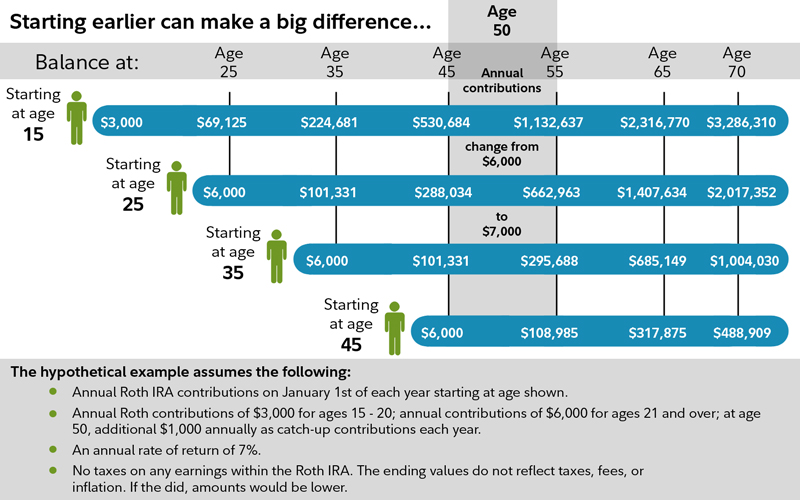

#2. Save with a Roth IRA

Traditional retirement accounts are appealing in-the-moment because they reduce your taxable income, but you may regret using them when retirement rolls around. Roth IRAs enable you to pay taxes on contributions now in exchange for tax-free growth in the future.

Roth IRA Benefits Based on Age – Source: Fidelity

If you have a traditional IRA, you may want to consider a conversion to a Roth IRA in order to realize tax-free capital gains from that point onward. The ideal time is when you fall into a low-income tax bracket, but it could make sense even in a higher tax bracket. Roth conversion calculations can be complex, but they often make the most sense for investors with long time frames, want to avoid distributions, and hope to leave the funds to their heirs.

Most retirees use Roth IRAs to supplement taxable income in order to remain in the lowest possible tax bracket. For example, you may target a tax bracket with an income limit of $50,000. If $50,000 isn’t quite enough to support your retirement needs, you could withdraw additional income through a Roth IRA without going over the limit.

#3. Harvest Your Losses

The market tends to rise over the long run, but every investor knows that there are short-term bumps in the road. While nobody likes these bumps when they occur, tax loss harvesting can help you take advantage of tax laws surrounding investment losses.

Tax loss harvesting is the process of realizing investment losses right now, which offsets any other capital gains or up to $3,000 in ordinary income during the current year. While there are some rules surrounding these practices, they may make sense for a lot of investors.

Note: The Wash Sale Rule requires you to wait 30 days before repurchasing an identical or substantially similar security in a stock portfolio.

#4. Donate to Charity

Charitable donations are a well-known way to generate write-offs for those that itemize taxes, but few investors realize that stock donations can be especially valuable. In addition to a write-off at fair value, donating stock enables you to forgo any accrued capital gains tax.

Donating stock that has appreciated for more than a year could be worth 20% more to a charity than if you sold the stock and made a cash donation since you avoid paying capital gains taxes. You can even donate stock that is not publicly traded, such as restricted stock or crypto assets.

Generating an Income

Many people face tough decisions when deciding when to retire. For example, you may want to retire earlier and decide that it’s worth the cost to incur early withdrawal penalties or decide to take Social Security earlier and forego higher levels of benefits.

There are several alternatives to these costly decisions:

- Part-time Job: Part-time employment can be a way to maintain social connections and provide extra income during early retirement years before you’re able to rely on full Social Security benefits or retirement plan accounts.

- Income Investing: If you have taxable accounts, income investing is a great way to generate a supplement income. Dividend stocks, high-yield bonds or income-generating option strategies are all viable options to generate an income.

The Snider Investment Method is designed to help investors generate an income using covered call options. While low interest rates have depressed bonds and equities can have lofty valuations, stock option income is relatively independent of the overall market and provides a way to generate a consistent income regardless of the macro environment.

Sign up for our free e-courses or learn more about our asset management services.

The Bottom Line

Retirement should be a time to relax and enjoy life, but that doesn’t mean ignoring taxes and investments. By keeping the four tips we’ve covered in mind, you can help minimize your taxes during retirement in order to help your income last longer and potentially provide a greater nest egg to your heirs.