Retirement is supposed to be a time for you to relax and enjoy the fruits of your labor over the past few decades. In reality, it can be a struggle to transition from working every day to living on a fixed income—especially if you struggle with creating and sticking to a budget.

Let’s take a look at how to downsize your budget in retirement to ensure a smooth transition.

Start with a Budget

About 80% of Americans use a budget, according to a Debt.com survey, but only about half of households stick to their budget. In addition, more than half of respondents budget with pen and paper rather than using mobile apps or financial advisors, which may be a lot more error-prone and time-consuming than modern budgeting methods.

Budgeting is a critical component of retirement planning because, after you’re retired, you cannot easily work an extra shift or put in overtime to pay off an unexpected bill. Most retirees live on a fixed income provided by a combination of Social Security, IRAs, pensions and other retirement assets, which means that expenses must be under control.

If you don’t budget or have trouble sticking to one, you may want to consider using a budgeting application that connects to your bank account. Some popular options include Mint, YouNeedABudget and EveryDollar, which all make it easy to import and categorize transactions without having to reconcile with your bank account.

Financial advisors can also help you optimize the income side of the budgeting process. For example, they can help you calculate how much you can afford to draw down each month, when to take Social Security or other benefits and help you weigh the costs of different actions on your retirement assets.

Pay Down Your Debt

Nearly 80% of American households between 55 and 64 have a median of $69,000 in debt and those between 65 and 74 still had a median of $42,000 in debt. While people spend and borrow less in retirement, nearly half of retirement households have at least $2,500 in credit card debt, according to Debt.org.

The problem with debt is that it consumes cash flow and puts other assets at risk. Every loan payment takes money away from your other costs of living, such as food or travel, while a failure to pay debt could lead to interest, penalties, bankruptcy or the repossession of assets. High-interest credit card debt, in particular, can lead to a debt spiral that’s difficult to exit.

If you’re struggling to pay down debt, start by avoiding the addition of any new debt to your existing balances. Stop using credit cards and avoid taking out any new loans. When tackling your existing debt, prioritize your highest interest debt to maximize the value of each dollar, or if it works better for you, try paying off smaller debts first for easy wins.

You may also want to consider debt consolidation as a way to reduce the amount you owe and even cut down on your monthly cash outflows. While this can be a great strategy to lower costs, it’s important to look at the fees and other terms associated with debt consolidation services since high fees and onerous terms can offset the benefits in some cases.

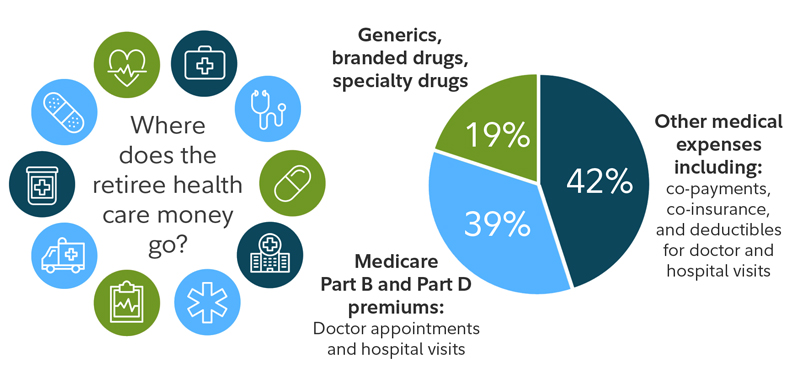

Manage Healthcare Costs

Fidelity estimates that the average couple will need $285,000 in today’s dollars for medical expenses in retirement, excluding the cost of long-term care (which can be even more extreme), making it one of the largest expenses in retirement. While these costs are difficult to reduce, ignoring them can throw your budget out the window.

Sources of Healthcare Costs – Source: Fidelity

Medicare offers many different options for health coverage. You may be better off paying a higher premium without paying out-of-pocket costs for each visit. You should carefully consider the cost of premiums and copays, as well as various supplemental insurance policies, to determine the best options.

You may also want to consider filling in any health care cost gaps with tax-advantaged accounts, including Health Savings Accounts, or HSAs. These accounts enable you to spend tax-free on health care in retirement, which is especially important if you’re retiring before Medicare kicks in, but helpful even in Medicare years.

Cut Down on Waste

Most people don’t spend hours each week pouring over their bank statements, so it’s natural that there’s a little waste built in to everyone’s budget. One survey of 1,000 Americans found that 64% of respondents admitted a considerable amount of wasteful spending that averaged $139 per month—a significant amount for anyone’s budget.

Wasteful spending encompasses many different areas of life, including budget line items like:

- Excessive or unnecessary fees.

- Impulse purchases.

- Unused or unnecessary subscriptions.

- Failing to return unneeded items.

- Using unnecessary energy.

- Frequent restaurant meals.

- Throwing away leftovers.

- Upgrading functional items to new models.

Cutting waste can improve your monthly cash flow by both eliminating outflow and opening the door to potential inflow. After all, you can invest any excess funds in securities that generate an income over time, which can actually increase your cash flow in retirement. And, you won’t be missing anything since many of these items are unused.

The easiest way to find opportunities to cut waste is to review your monthly bank or credit card statements and see where your money is going each month. You can also use online services, like Truebill, to identify unused subscriptions and track your spending—it even tells you when you may be able to negotiate some bills lower!

Study Your Housing Costs

In many cases, homes are one of a retiree’s largest assets. However, they also likely account for a significant portion of their monthly expenses. Taxes, maintenance, and repairs quickly add up, especially on older homes. Make an honest assessment of your housing needs. Are you still using your entire home? Does a more tax-friendly state make sense? Could renting be the best choice in retirement? You can read more about downsizing here.

The Bottom Line

There are many different ways to downsize your budget in retirement. In addition to these strategies, you may want to look at ways to boost the other end of the equation—your income. Some investment strategies enable you to generate more income from your existing retirement assets.

The Snider Investment Method is a long-term strategy designed to create income from your portfolio and ensure cash flow in retirement. It uses a combination of stock, options and cash, along with specific techniques applied in a specific sequence, to maximize your portfolio’s income potential.

Sign up for a free e-course to learn more or explore our asset management services for a hands-off approach.