Many investors rely on dividend-paying stocks to fund at least part of their retirement. When budgeting for income and expenses, it’s helpful to know how much you can expect from dividends. The problem is that dividend payments vary each quarter and aren’t always a guarantee. Not to mention that your after-tax dividend income depends on a variety of different factors.

Let’s take a look at how you can accurately estimate dividend income, as well as some tips for generating stable income in retirement.

Dividend Income Strategies

Dividends are a popular form of investment income because of their low tax rate compared to fixed income. While interest is subject to ordinary income tax rates, dividends are typically subject to lower long-term capital gains tax rates. The trade-off is that stocks are riskier than bonds, and the income tends to fluctuate over time.

Living off dividend income is tricky because you have to balance income with risk. It’s tempting to buy high-yielding stocks to support a higher level of spending, but these stocks tend to be more volatile than blue-chip stocks that offer a lower yield. So the safest bet for most investors is using dividends as only one bucket of income in retirement.

For example, you might have Social Security income, pension income, fixed income, and even income from other sources, like covered calls. A portfolio of dividend stocks adds to and diversifies these different sources of income while providing the greater returns of stock ownership (along with covered call strategies that do much of the same).

Projecting Dividend Income

Dividends tend to fluctuate year to year depending on a variety of factors. For example, a real estate investment trust, or REIT, may pay out a set percentage of its profit as a dividend. If rents decline over the course of a year, these dividend payments may shrink. The same goes for oil companies, utilities, or other cyclical or volatile businesses.

You can roughly calculate how much you’ll receive by multiplying the number of shares you own by the dividend amount per share. For example, if you own 100 shares of stock and the quarterly dividend amount is $0.10 per share, you will receive $10.00 in quarterly dividends or $40.00 per year, assuming that the dividend remains the same for four quarters.

Preferred stock dividends work a little differently. To calculate how much you’ll receive, multiply the dividend yield by the stock’s par value and then multiply that amount by the number of shares that you own. For instance, if you own ten shares of preferred stock with a par value of $50 per share and a 10% yield, the dividend payment will be $50.00.

When projecting dividend income, it’s essential to look at your after-tax income since that’s the amount that you’ll actually take home and spend. Dividends are either qualified or non-qualified depending on the stock and the amount of time you’ve held it—and there’s a big difference in the tax rate for each option.

- Qualified dividends are subject to long-term capital gains taxes, which are 15% for most investors. Most dividends paid by U.S. companies trading on U.S. exchanges, such as the NYSE or NASDAQ, are qualified dividends.

- Non-qualified dividends are subject to ordinary income tax rates, which tend to be much higher. Examples of non-qualified dividends include REIT dividends, MLP dividends, preferred debt, or dividends as part of an employee stock ownership plan.

You can calculate your after-tax dividend income by multiplying your tax rate by your dividend and subtracting that number from the total dividend income. For example, a qualifying dividend of $50 may be subject to a 15% tax, yielding an after-tax income of $42.50. The $42.50 figure is the amount that you ultimately take home and spend in retirement.

Using Dividend Calculators

Calculating dividend income from a single stock is pretty straightforward, but tracking an entire portfolio is challenging. In addition to making multiple calculations, you need to keep track of dividend changes across every stock each quarter to ensure accurate estimates. Fortunately, dividend calculators can help automate the process.

The most common way to calculate dividends is using a spreadsheet. But, a portfolio can quickly out grow a spreadsheet. If you aren’t familiar with Excel or Google Sheets, there is a learning curve. Spreadsheets also mean you need to manually update your portfolio and any changes with your holdings, dividend payments, or dividend dates. Fortunately, there are many better options that tracking your dividend portfolio is a spreadsheet.

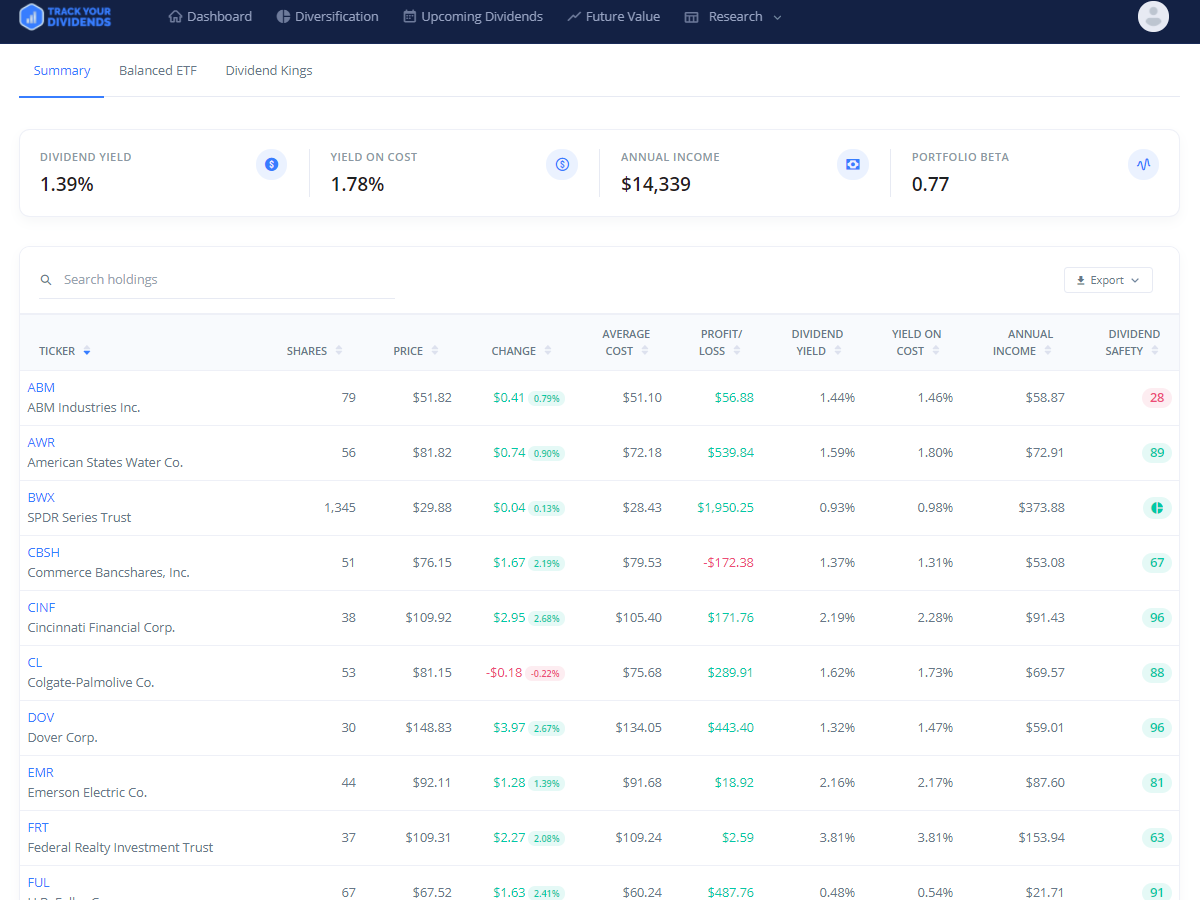

TrackYourDivdiends.com’s helpful user interface. Source: TrackYourDividends

TrackYourDividends.com provides a free dividend calculator that projects income growth over several years. If you’re looking for more, the tool enables you to link your brokerage account and see a complete analysis of your dividend income stream. You can also access tools to help identify opportunities and maximize your income.

These tools include:

- Proprietary ratings and top Wall Street analyst opinions to ensure that you’re holding high-quality stocks.

- Dividend analyses that break down yield history, payout ratios and provide a dividend safety score.

- Competitor analysis to see how your stocks measure against alternative dividend-paying stocks.

- Valuation tools to help you find undervalued companies that also pay substantial dividends—the best combination for success.

Try the dividend calculator or sign up for a free account to link one brokerage and start analyzing your dividends.

The Bottom Line

Many investors rely on dividends to fund at least a portion of their retirement needs. While tracking and estimating dividend income is challenging, TrackYourDividends.com and other tools help automate the process by connecting with your brokerage account, importing your portfolio, and running calculations to help you track and optimize income.

If you’re interested in generating income beyond dividends, the Snider Investment Method provides a turnkey strategy for generating income from covered call options. Take our free e-course to learn more or inquire about our asset management options.