Suppose that you were ready to retire in 2007 with a $1 million stock portfolio. At a four percent withdrawal rate, you would have $40,000 per year in income. However, the 2008 financial crisis decreased the portfolio’s value to just $600,000 and the same four percent withdrawal rate left you with just $24,000 per year in income — not enough to retire.

Most investment advisors recommend reducing portfolio risk as you approach retirement to prevent these kinds of situations. For example, you may allocate a greater percentage of your portfolio to less volatile investments, such as bonds, to weather poorly timed market corrections. This helps create a more stable valued portfolio, making retirement planning easier and avoiding the possibility of delaying retirement.

Let’s take a look at a few instances where this advice doesn’t hold true and some alternative strategies to consider.

How to Ensure You Won’t Run Out

It’s no secret that most Americans don’t have enough saved for retirement. According to Bankrate, Americans between the ages of 55 and 64 have saved just $120,000 — that’s only 12 percent of the $1 million that many experts recommend. These individuals may not be able to catch up to their retirement goals without taking on more risk than advisors would recommend.

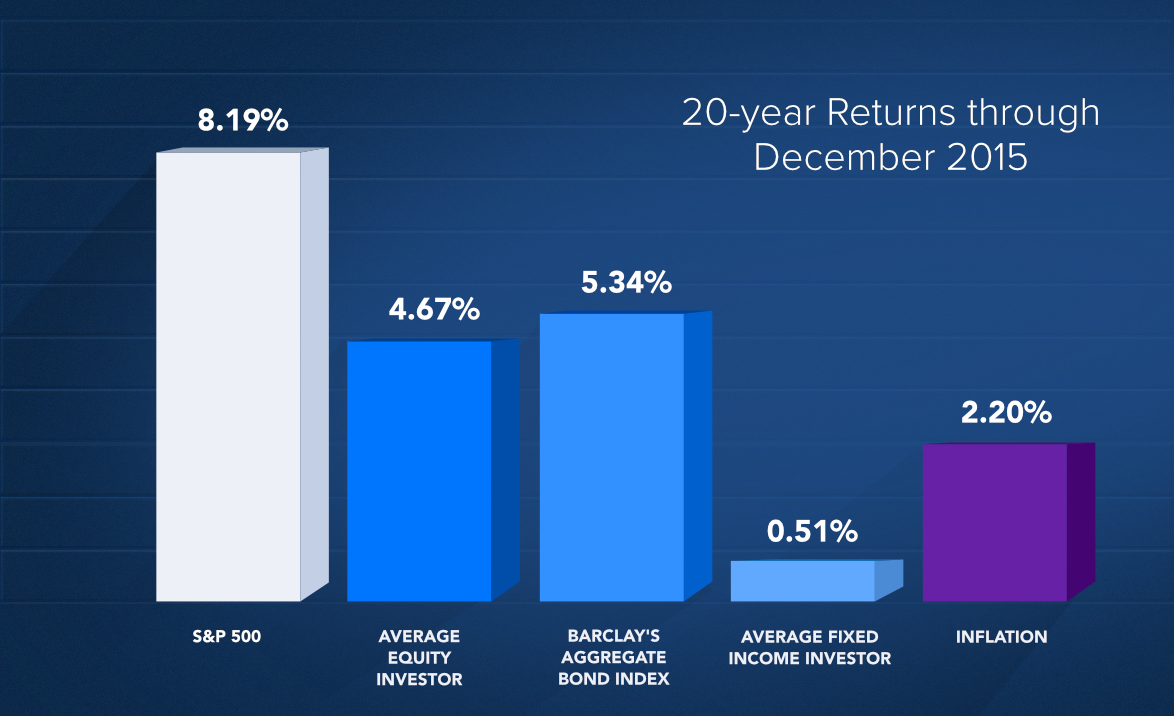

For example, a stock portfolio might return six percent per year, but a bond portfolio would be hard-pressed to match those returns. If you require a six percent return per year to reach your retirement goals on-time, you may need to consider allocating more capital to stocks than many advisors would recommend — particularly if you’re very behind.

There’s also the risk that you could live longer than the average person. While everyone wants to live longer, a longer lifespan translates to higher costs. If your portfolio drawdown assumes an average lifespan, you could run out of money if you live longer than the average person. You may need to take on greater risks in some cases to meet these new requirements.

The idea of reducing portfolio risk as you approach and enter retirement was created in a time when most people passed away shortly after retiring. That is no longer the case today. It is not uncommon for one spouse in a healthy couple to spend over 30 years in retirement. A longer time frame allows investors to handle more risk. It also means their assets need to keep producing for a significantly longer period of time.

The best way to avoid these problems is to start saving more money earlier, but at a certain point, that isn’t a practical solution to the problem. You may require more creative ways to generate sufficient income from existing retirement assets rather than focusing on accumulating more assets when you’re no longer able to work.

Realizing the Best Risk-Adjusted Returns

There are other instances where you may have saved too much money for retirement. While this is a good problem to have, it doesn’t make sense to sacrifice potential returns if you don’t plan on withdrawing the capital. You could invest in riskier assets to increase portfolio returns and leave more money to future generations or charities after you pass away.

Start by determining how much you need for retirement and ensure that the capital is invested widely. With the remaining capital, you can invest in riskier assets that will generate higher returns over the long run, such as growth or international stocks. This lets you optimize your portfolio’s long-term returns without putting any capital that you do need at risk.

A related problem is focusing too much on risk or return without looking at risk-adjusted return. For example, Treasury bonds may have very low risk, but they don’t have an optimal risk-adjusted return. You may be able to find better investments that offer greater returns for each unit of risk or volatility, such as municipal bonds or blue-chip dividend-paying stocks.

Alternative Strategies to Consider

There are many ways to generate more income during retirement without taking on excessive risk by moving into stocks. If you’re behind on retirement and still want to retire on time, it’s worth exploring ways to generate greater income from an existing portfolio rather than trying to grow the portfolio enough to support the same income generation.

For example, assume that you have a $500,000 retirement portfolio and require $25,000 per year in income. The money would only last about 20 years if invested in conservative assets that were sold off to finance retirement, but generating a higher level of income from the $500,000 in assets could change those dynamics.

The Snider Investment Method focuses on writing covered call options to generate a consistent income during retirement. By selling call options against a portfolio of stocks, you can generate an income above and beyond dividends or fixed-income investments. You also benefit from the greater inflation protection of owning stocks rather than bonds.

Our goal with the Snider Investment Method is to enable you to achieve the returns realized by the stock market while reducing some of the risk. We optimize the portfolio by selling call and put options to boost income that can support you during retirement with minimal effort.

The key to success is taking emotion out of the process and finding ways to automate the process. Using our unique strategy, you can follow a specific set of rules in just a few hours each month. You can even use our streamlined tools and Lattco platform to execute these trades without worrying about finding screeners or other tools.

Sign up to take our free introductory courses to learn more about writing covered calls and how you can supplement your retirement income.

The Bottom Line

Many financial advisors recommend decreasing risk as you age, but that’s not always the right decision. If you are at risk of falling short of your retirement goal or are saving too much, you may be better off investing in riskier assets to make up the difference and/or optimize your risk-adjusted returns. You may also want to consider alternative strategies, such as options.

Sign up for our free introductory courses to learn more about how covered call options can help you generate retirement income without resorting to dividend stocks or bonds. If you would prefer a more hands-off approach, we also offer conventional asset management services.