More than half of Americans who are within 20 years of retirement expect to retire with less than $100,000 in their savings, according to MoneyRates.com. Even if you have $100,000 to $500,000 saved for retirement, you may be wondering if it’s enough to finance retirement, and if not, how to catch up to the right number.

Let’s take a look at how much you really need to save in retirement, how to stick to a budget, ways to improve portfolio yield and whether you should work a little longer.

Are you behind on your retirement savings? Try these strategies to catch up!

How Much Do You Need?

The amount of money that you need in retirement depends on your portfolio return and yield as well as retirement income requirements.

Many financial advisors recommend saving enough to replace 70% to 90% of your annual pre-retirement income with Social Security and investments, but your exact requirements may vary based on your individual circumstances. For example, you might pay off your mortgage before retirement and have significantly lower housing costs in retirement.

The average annual return and yield of an investment portfolio also varies considerably from person to person. In general, a conservative portfolio might return five percent per year. You can either draw down the portfolio to finance retirement spending or plan to live off of the income generated from fixed income investments, dividends and other sources.

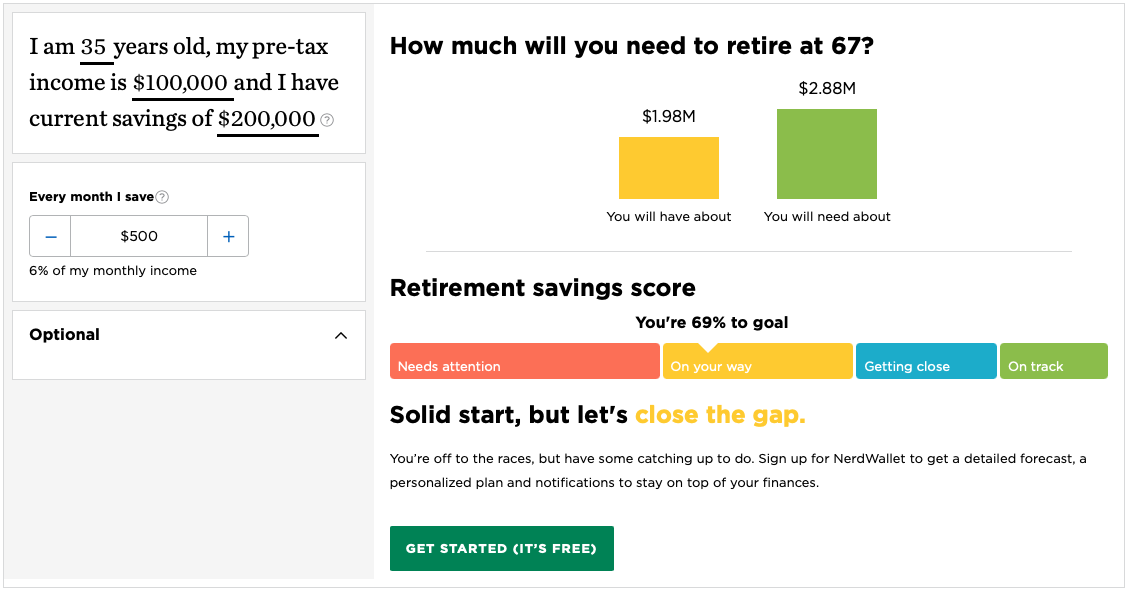

Retirement calculators can help you estimate how much money you should save each month in order to achieve a desired level of spending in retirement. NerdWallet, SmartAsset, BankRate and AARP are all excellent retirement calculators that factor in inflation, salary, portfolio returns, and portfolio yield to come up with estimated saving requirements.

Start (and Stick to) a Budget

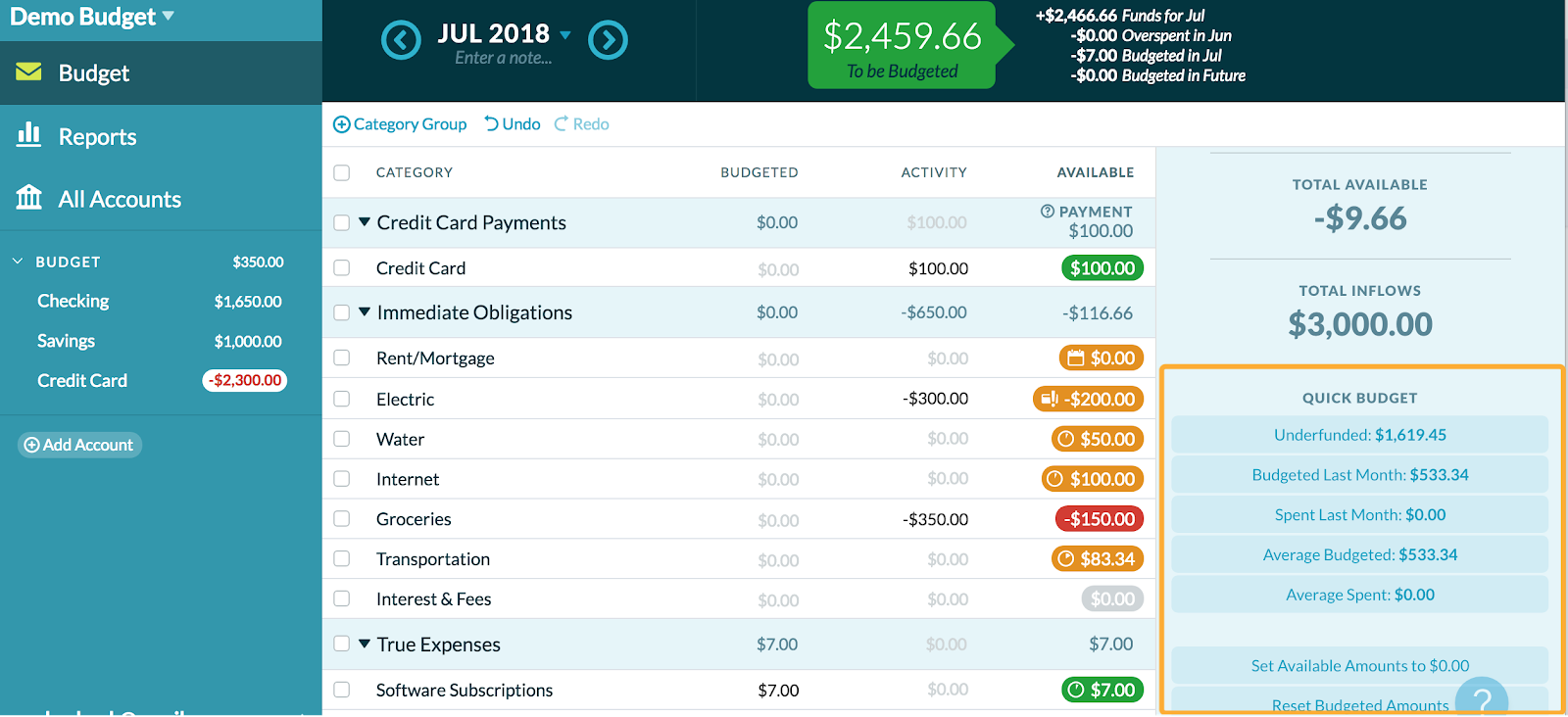

Budgeting is one of the most important steps to take to catch up on your retirement savings. By cutting spending, you can increase the amount of money that you have left over to save for retirement and prove that you can live on less money in retirement. While 80% of Americans use a budget, according to Debt.com, less than half of them stick to it.

There are several popular budgeting strategies:

- Envelope Budgeting: Envelope budgeting involves allocating income into different “envelopes” or categories of spending. For example, you may divide a $1,500 paycheck into $500 for rent, $500 for transportation, $250 for groceries, and $250 for retirement savings. As a rule, you cannot spend money that’s not in the envelopes.

- Zero Budgeting: Zero budgeting starts with your monthly income and finds a place for every dollar before it hits your bank account. That way, you don’t have to stress about where money is going when it hits your bank account, and you can plan ahead to ensure that you’re making the best use of every dollar.

- 50/30/20 Budgeting: The 50/30/20 budget is designed for people that have excess income and have already paid off most of their debt. Rather than saving every last penny, the strategy encourages 50% spending on necessities, 30% spending on fun money and 20% spending on debt reduction, savings and investments.

Modern web and mobile apps have made it easier than ever to create and stick to a budget. Mint, PocketGuard, You Need a Budget, Wally, Mvelopes, Goodbudget and Personal Capital are all excellent options for creating a budget and following through with it—especially because they can automatically interface with your financial accounts.

Increase Your Portfolio Yield

Many retirees aim to—at least partially—live off of their portfolio yield rather than drawing down their portfolio. For example, an investor might own a $1 million portfolio of fixed income investments that pay a 3% annual yield—or $30,000. The $30,000 in income each year doesn’t involve selling any of the principal fixed income investments.

There are several ways to generate yield:

- Fixed income investments, like bonds, pay regular coupon payments.

- Dividend stocks often pay quarterly dividends to shareholders.

- Real estate investments may pay monthly rental income to partners.

- Energy limited partnerships make regular distributions to partners.

The downside of these investments is that they typically have less growth potential than equities and aren’t nearly as liquid. For example, it’s harder to sell a rental property than a stock, many dividend-paying stocks are in slow-growth industries (e.g., utilities), and bonds aren’t exactly known for their capital appreciation over time.

The good news is that there are several alternative ways to increase portfolio yield. For example, covered call options provide investors with a way to generate an extra income on top of an existing stock portfolio. The Snider Investment Method details our unique approach to selecting the right stocks and finding attractive covered call option opportunities.

Sign up for our free e-course to get started!

Consider Delaying Retirement

There are some cases where budgeting and investment strategies alone aren’t enough to reach your retirement goals. In that case, you may need to consider delaying retirement or finding a part-time job during retirement to supplement your income. This is especially true if you retire before Medicare coverage kicks in since many employers provide health insurance.

There are several reasons to work a little longer:

- Save on health insurance.

- Contribute to your retirement savings.

- Pay off debt to increase cash flow.

- Increase your Social Security benefit.

- Maximize your spending power.

If you choose to retire from full-time work, part-time jobs are a great way to earn a little extra income and potentially realize some of the same benefits. For example, you may be able to buy health insurance at a lower price than the marketplace and delay taking Social Security in order to increase your permanent benefit down the road.

The Bottom Line

Many people feel insecure about their retirement savings. While financial advisors may recommend multi-million-dollar portfolios, the actual amount that you need in retirement varies considerably from person to person. There are several online tools that you can use to assess your retirement income requirements, or you can speak to a financial advisor.

If you determine that you haven’t saved enough, you may want to get more serious about budgeting, explore ways to increase your portfolio yield or consider working a little longer to get on more solid financial footing before retirement.